Why the Vertical Gas Corridor Will Not Operate at Its Full Potential

The Rupcha-Vetrino Pipeline Reduces – But Does Not Remove – the Main Bottleneck Limiting Bulgaria’s Transit Potential

Many of the developments surrounding Bulgartransgaz projects remain poorly understood not only by the wider public but also by a significant number of energy policy observers. The reason is simple: in the energy sector, things are rarely what they appear at first glance.

This is particularly true in Southeastern Europe, where official explanations often conceal deeper economic, political, and geopolitical realities.

When the issue at stake is the reconfiguration of European gas flows following Russia’s invasion of Ukraine, the debate is no longer merely about infrastructure or commercial interests. It is about influence, security, and the future balance of power in Europe’s energy market.

At its core, the contest is straightforward: will Russian gas maintain its dominant position – directly or indirectly, through blending, rebranding, and alternative transit routes – or will non-Russian supplies gradually displace it from the markets of Central and Eastern Europe?

It is therefore no coincidence that recent meetings between U.S. representatives and Bulgaria’s political leadership have increasingly focused on the country’s transit role. Bulgaria remains a pivotal battleground in the competition between Russian and non-Russian gas for access to European markets.

What Is the Vertical Gas Corridor?

The Vertical Gas Corridor is a project of strategic importance for both the European Union and the United States.

Its purpose is to establish a reliable route for non-Russian natural gas – primarily LNG imported through Greece – to Romania, Moldova, Ukraine, Slovakia, Hungary, and the wider Central and Eastern European region.

The strategic rationale is straightforward: create a viable alternative to Russian gas supplies and gradually dismantle one of the Kremlin’s most effective instruments of political influence in Europe.

Support Independent Analysis

Help us keep delivering free, unbiased, and in-depth insights by supporting our work. Your donation ensures we stay independent, transparent, and accessible to all. Join us in preserving thoughtful analysis—donate today!

Every project associated with the Vertical Gas Corridor should therefore be evaluated against a simple criterion: does it materially increase the capacity available for transporting non-Russian gas to Central and Eastern Europe?

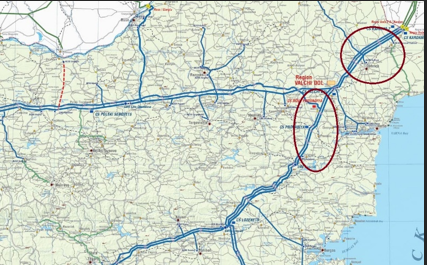

Where Was the Bottleneck?

Until recently, the corridor faced two major obstacles.

The first was economic. Transmission tariffs along the route significantly undermined the commercial viability of deliveries to downstream markets.

The second was physical. Insufficient reverse-flow capacity along the Trans-Balkan Pipeline created a major infrastructure bottleneck.

This is where Bulgaria became the corridor’s most critical constraint.

Following the construction of TurkStream, Bulgartransgaz repurposed sections of the existing Trans-Balkan Pipeline infrastructure between CS Strandzha and CS Provadia to serve the new export route toward Serbia.

As a result, a substantial portion of the capacity of the Kardam-Negru Voda 2 and 3 lines became effectively unavailable for alternative deliveries to Romania and further into Central Europe.

While Russian gas enjoys access to more than 57 million cubic meters per day of entry capacity via TurkStream through Strandzha 2, competing non-Russian supplies arriving from Greece and Turkey continue to face significant restrictions.

The Response from Brussels

Following the commissioning of TurkStream, the European Commission sought ways to offset the resulting imbalance.

It was in this context that the Rupcha-Vetrino looping project emerged.

The project received strong political backing from Brussels and was included among the initiatives for which Bulgaria sought support through the EU Modernisation Fund as part of the broader development of the Vertical Gas Corridor.

The objective was straightforward: restore part of the transmission capacity lost to the TurkStream configuration and increase northbound flows of non-Russian gas.

Why the Current Rupcha-Vetrino Project Does Not Solve the Problem

According to public statements by Bulgartransgaz management, once the Rupcha-Vetrino loop is completed, approximately 27 million cubic meters per day of capacity will be available toward Romania through Kardam-Negru Voda 1.

This undoubtedly represents an improvement.

But it does not represent a solution.

More than 57 million cubic meters per day of capacity were effectively removed from the system and redirected to support TurkStream operations. The new project restores only about 27 million cubic meters per day, resulting in a modest increase in export capacity toward Romania.

Moreover, the project has already been delayed, with completion pushed from the first quarter of 2026 to the third quarter of the same year.

The result is simple: less capacity and later delivery than originally anticipated.

Most importantly, the project does not envisage the restoration of commercial operations along Kardam-Negru Voda 2 and 3. This remains the principal limitation of the current design.

The bottleneck is therefore not eliminated.

It merely becomes smaller.

The Capacity Gap Still Matters

The significance of this limitation becomes clear when viewed in a broader regional context.

Prior to the reconfiguration associated with TurkStream, the Kardam-Negru Voda corridor was capable of handling volumes broadly comparable to the capacity now reserved for Russian gas transit through Strandzha 2 – more than 57 million cubic meters per day.

The Rupcha-Vetrino project restores less than half of that volume.

At the same time, demand across Ukraine, Moldova, Romania, and Central Europe continues to far exceed the incremental capacity being added. Even after the wartime decline in consumption, Ukraine alone remains one of the largest gas markets in the region.

In practical terms, the new infrastructure improves flexibility but does not create the scale necessary for the Vertical Gas Corridor to emerge as a fully competitive alternative to Russian supply routes.

This is why the future of Kardam-Negru Voda 2 and 3 remains so important. Their commercial reactivation would not merely add capacity; it would fundamentally alter the economics of the corridor by enabling larger volumes, greater supplier competition, better utilisation of LNG infrastructure in Greece, and a more robust diversification pathway for Ukraine and Central Europe.

Viewed from this perspective, Rupcha-Vetrino should be understood not as the completion of the Vertical Gas Corridor, but merely as one step toward its realization.

The Questions That Remain Unanswered

This raises a number of questions that have yet to receive convincing answers.

Why does a project presented as strategically vital for Europe’s diversification effort fail to restore the full capacity that was redirected to accommodate TurkStream, despite state guarantees approaching €500 million and additional requests for financing from the EU Modernisation Fund and U.S. financial institutions?

Why is there so little public discussion of the actual potential of Kardam-Negru Voda 2 and 3, whose reactivation could fundamentally alter the economics and scale of the Vertical Gas Corridor?

Why does Russian gas continue to enjoy virtually unrestricted access to existing infrastructure while alternative supply routes advance more slowly and under less favourable commercial conditions?

These are not merely engineering questions.

They are questions about whether Europe is pursuing genuine diversification or merely the appearance of diversification.

For non-Russian gas to compete successfully with Russian supplies, it must have access to comparable transmission capacity, equivalent market access, competitive tariffs, and sufficient time to establish itself in regional markets.

Without those conditions, diversification remains largely rhetorical.

The Strategic Test

The ultimate question is whether Bulgaria can realistically fulfil its proclaimed role as a key transit hub for Romania, Moldova, Ukraine, and Central Europe if a substantial portion of the infrastructure constraints remains in place even after the completion of the Rupcha-Vetrino section.

Diversification is not achieved through declarations.

It requires available, competitive, and commercially accessible transmission capacity.

If significant portions of the export potential of Kardam-Negru Voda 2 and 3 remain unavailable after the project’s completion, then the central constraint on the Vertical Gas Corridor will remain unresolved.

At that point, policymakers and market participants alike will have to confront an uncomfortable question:

Are we witnessing a genuine acceleration of diversification, or a carefully managed process that creates the impression of change while leaving the underlying dominance of Russian gas largely intact?

Ilian Vassilev