Alternatives & Analyses: The Southern Gas Corridor integrates SEE countries into EU’s gas market.

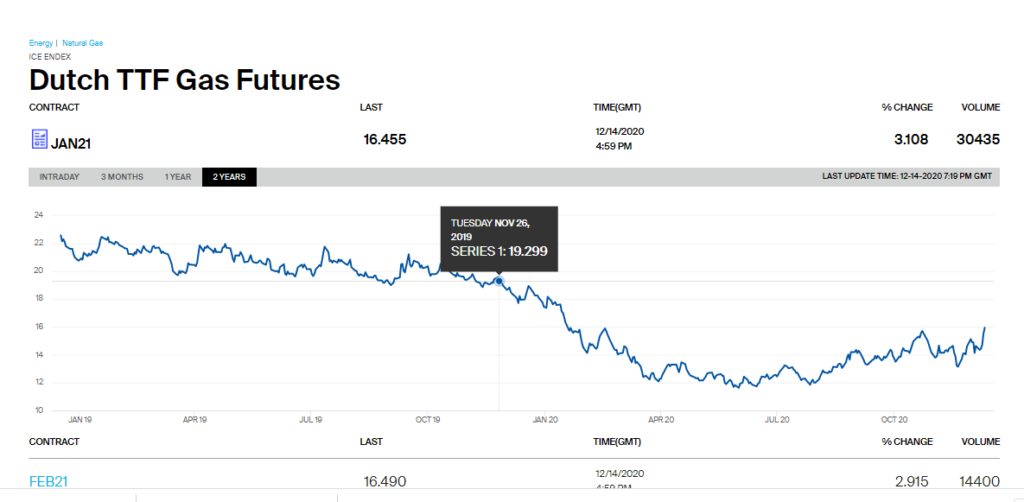

It is already clear that this winter season natural gas prices will remain below 2018 and 2019 price levels / see chart /

EU gas prices have risen to 16 euros per MWh this week, along with increasing consumption due to colder weather. Other factors also contribute, such as shrinking LNG production and exports from the United States, amidst typical market speculations in anticipation of rising prices.

More contributing factors are worth watching, that could impact future gas prices in the EU.

First, expectations for a milder winter in Europe will play a key role. The weather forecast made in mid-December does not offer a credible lead into what temperatures will be in mid-February, let alone March. Still, the quantities of natural gas stored in UGS across the EU and most notably in Ukraine certainly make up for some uncertainties in the long-term predictions. As the winter season advances, the pressure to dispose of gas stocks mounts, offsetting insurance concerns of cold spells. The protracted storage of natural gas in underground storage facilities adds to its cost, while the proximity of spring makes traders nervous.

These articles analyses and comments are made possible thanks to your empathy and contributions, which are the only guarantors of independence and objectivity in our work. The Alternatives and Analysis team.

Second, the COVID-19 crisis is yet to trigger critical scenarios for natural gas consumption. Winter is concurrently a “high” season for all cold and flu viruses, including coronaviruses, henceforth it is the season with the economy (? Don’t understand) and related energy demand most heavily affected by adverse health conditions.

In Bulgaria, the ratio between industrial and household consumption is approximately ten to one, which means that the economic consequences and a slowdown in economic growth have a more significant and direct impact on energy consumption levels. Worth the caveat – district heating companies are treated as industrial consumers.

Third, there is a growing likelihood of a change in the gas price formula in the supply contract with the Azerbaijani Gas Supply Company before the end of the year and certainly before the start of supplies on January 1, 2021. This could further help synchronize gas price levels between Bulgaria and its adjacent markets – Turkey, Greece and Romania. As in previous years, seasonal price fluctuations in gas spot markets in the high season make fully or partially oil-indexed natural gas more competitive.

Reference – at present, gas prices at the most liquid EU natural gas exchanges hover around 16 Euros / MWh. In comparison, the price for Russian gas under the supply contract between Gazprom and Bulgargaz is slightly above 14 Euros / MWh, i.e. Russian gas is more cost-competitive. The situation is unlikely to change dramatically after January 1, as the benchmark for oil indexation – Brent oil prices with six months lag will not have changed much. This analysis is valid only for current market snap analyses and does not cover longer-term strategies that rely on larger purchases and subsequent storage of cheap summer gas.

As previously noted, the main reason why the cheapest gas in Europe is currently supplied in Ukraine is that the country is one of the few that can store all the gas necessary for its annual consumption in its own UGSs. Bulgaria could potentially do the same, completely hedging against price fluctuations, if Bulgartransgaz adds 2.5 billion cubic meters as storage capacity in the Chiren UGS and elsewhere – an entirely feasible task.

In conclusion, despite the current barriers to the region’s full integration into the European gas market, the processes of market liberalization, synchronization and alignment of supply terms, including prices, trade, transportation, are in full swing.

Despite Moscow’s hectic attempts, Eastern Europe has every chance to profit from abundant cheap gas as much as Western Europe, which makes all geopolitically-induced projects meaningless, including those that bypass Ukraine.

With or without the EC’s or EU funding supporting the consumption of natural gas or its derivatives (such as hydrogen) as the best transition fuel towards a carbon-free economy, its place as a primary energy source is indisputable.

Ilian Vassilev

Thank you for your donnations via PayPal and bank transfers to IBAN BG58UBBS80021090022940