Vladimir goes global – Part 1

Negative energy

Russian leader Vladimir Putin, frustrated in his war on Ukraine, is in apocalyptic mood and is attempting to win that war by globalising it. Recent events in the Middle East are partly diversionary and partly an attempt to upgrade a “Russian energy weapon” that, in its classic Eurocentric version, hasn’t worked because the West has been unexpectedly resilient – and become more so in the course of the last two years. For a variety of reasons, Mr Putin’s latest ploy won’t work either. In the first part of this two-part article, having briefly contemplated the Apocalypse and why Mr Putin should be willing to risk it, we look at reasons in the realm of energy why his bet is destined to fail.

Whoever said that globalisation was dead? Nonsense! It’s alive and well – and living in the Kremlin. And its main proponent is none other than Russian president Vladimir Putin. True, this is globalisation of a particular sort: the globalisation of conflict. But, in accordance with the old business-school maxim, Mr Putin is “thinking global and acting local”.

And there’s another resonance. The whole thing is reminiscent of Russian revolutionary leader Vladimir Lenin’s first attempt at using globalisation as a foreign policy tool. Remember “Workers of the world unite!”, the slogan of Marx’s Communist Manifesto? Well, this time it’s “Autocrats of the world unite!” But Mr Putin’s enemy remains the same as Comrade Lenin’s – the democratic and capitalist West. Time and again, Russia is triggering and benefitting from “regional” conflicts to engage the West on a broader and broader front. The aim is to divert attention from Moscow’s war in Ukraine, stretch the West’s resources and sap Western support for Kyiv, while engaging allies and partners in Kremlin’s confrontation. Which is a global aim in a way: if that war succeeds, the “reclaiming” of Ukraine will be the first step in the restoration of Russia to its rightful place as a global power. And if it fails, well, so much the worse for the globe…

Recent tensions and hostilities in the Red Sea, involving Yemen’s Houthi rebels, are just the latest instance of this pattern. The activation of the Gaza-based Palestinian group Hamas and its attack on Israel on October 7 last year had an identical purpose. And it’s not just a question of shifting global attention away from Ukraine. Mr Putin also seeks to frame his war there as part of a broader conflict between the West, on the one hand, and Russia, backed by the Global South, on the other.

The Kremlin has resorted to tactics of this kind several times in the course of the war. It started with moves in the Western Balkans, via Kosovo and Republika Srpska. It continued with attacks in Syria and Iraq. And then it proceeded to Africa, fomenting trouble in countries stretching from Sudan to Mali. Essentially, Moscow has been acting wherever it could escalate a simmering conflict and involve the West. Next in line is Venezuela, then Latin and Central America.

The Putin regime has also been striving to globalise the conflict in a slightly different way, by activating military-technical cooperation with North Korea. This has served two purposes. It has, lately, given Russia a battlefield advantage in munitions and it has also heightened North Korea’s aggressive rhetoric toward South Korea, the United States (US), and Japan.

Plot these points of tension, both old and newly activated, on a map of world, and it will be pretty clear what Moscow is up to. It is trying to plunge the world into a new global war.

This, of course, assumes that, broadly speaking, it’s Mr Putin who has been making the running in the Middle East in recent months. I think there’s good evidence – as good as anyone can access at present who isn’t an intelligence agency official – to believe that this is the case. But that’s an intricate argument and I will postpone it to the second part of this two-part article.

If you like this article, please support us with a donation to PayPal and to the direct account of the association Alternatives and Analyses IBAN BG58UBBS80021090022940. This will ensure that there will be further analyses

Mr Putin recognises that he is unlikely to win the war in Ukraine – he does not have the resources – but he cannot afford to relinquish military power because he sees it as the very foundation of Russia’s existence. And perhaps he’s right, at any rate as far as the Russia he has inherited and the Russia he wants are concerned. The resort to militarisation of public life is a classic move of Russian “statecraft”, very much in line with Russian autocrats’ traditional methods of retaining power at home and projecting it abroad. It serves as a distraction from economic and social woes that the Kremlin is unable to resolve by economic means.

Whether for reasons of politics or of simple biology, Putin will sooner or later leave power. However, before that, he appears intent on shaking the world and pushing it into war in the highest-stakes gamble of his life – either leave the world and Russia in ruins or leave his imprint on history as the Great Leader and re-uniter of the Russian Lands. And for now, the chances are that his legacy will be a grim one of instability.

Après Poutine, le déluge…

Now, why should Mr Putin be feeling so desperate and apocalyptic just now? Why should he be upping the stakes? He not concerned about losing his presidency, the elections outcome is preordained. It is history and his skin-deep knowledge of how Russia disposes of failed Tzars.

Well, it’s also a matter of the situation on the battlefield. Though Ukraine’s counter-offensive has certainly not lived up to expectations, the current bloody and immobile war of attrition does not give obvious promise of anything that the man in the Kremlin could plausibly claim as a victory, except in the event of a radical failure of nerve and will in the West. Yet the EU has not only just voted in a €50 billion package for Ukraine – which had been disputed, if only by Hungarian strongman Viktor Orban. More importantly, it has also retuned its policies and economy to meet the direct military threat from Russia.

Mr Putin’s moves are also partly – and perhaps more importantly – due to his silent admission of the fact that Russia’s “energy weapon” has been successfully defused. Either the West has found effective counter-measures to it. Or it was never as formidable as many, surely including Mr Putin, thought in the first place.

It’s a point that deserves expansion. And, in the course of that expansion, we can touch on a slightly different point.

Recent moves might perhaps also be seen as, secondarily, an attempt to enhance or upgrade that “energy weapon”, by using troubles fomented in the Red Sea to squeeze the West’s energy supplies in ways additional to those Mr Putin first thought of.

If so, an immediate “spoiler alert” is in order: it won’t work; it can’t work; and it’s a ploy that will rebound on Mr Putin in two ways. First, in terms of revenue flows, And, second, because it will alienate many of the players who are (actually, potentially, or in Vladimir’s dreams) on his team in the Great Game of global geopolitics. But we’ll get to all that eventually.

For now, consider first how shock-proof the international economy appears to have become.

Shock-proofing

Remember how natural gas prices surged in the wake of the invasion of Ukraine in February 2024? Well, there’s been nothing remotely similar by way of reaction to recent events in the Middle East. That’s a novelty. And it means something.

Thus, crude oil prices were actually 10% lower in the month following the Hamas attack of October 7 than they had been before it. Reason? Mainly that North American production of crude reached new record levels, its growth compensating for the production cuts agreed by the OPEC+ countries.

Admittedly, prices of the world’s two key benchmark grades – West Texas Intermediate (WTI) and Brent – have since risen, largely because of Red Sea specs and depletion of the Strategic Reserves of the US. But the market has hardly gone well beyond $80/bbl and is unlikely to go much higher than that. The market will need to experience a much greater geopolitical shock – possibly nothing short of a new war in the Middle East – to return to its old trajectory of oil price growth. Saudi Arabia has been playing ball with Russia to keep prices high, but it has quietly joined Mr Putin and his marvellous energy weapon in their fate: the world economy has developed a higher resilience threshold by being almost permanently subjected to the supply-disruption measures of OPEC+.

Again, consider stock markets. Stock prices on the world’s leading bourses did not fall substantially following the initial Houthi attacks on oil and LNG tankers in the Red Sea.

The conclusion to be drawn from this is that global markets are exhibiting a degree of flexibility that enables them to manage even significant geopolitical upheavals. Two things might be added to this. First, as we shall see, the period required to adapt to such shocks is getting shorter. And, second, in times of uncertainty global capital seeks safe harbours in the West: which means that it punishes warmongers – and their friends. Even Chinese stock markets are suffering

(see chart). Which is bad news for Moscow. For Russia craves China’s goodwill. And Chinese leader Xi Jinping craves economic growth – which is being imperiled by Western disinvestment in the Chinese economy.

Back to the West, however. What’s the source of this resilience?

Well, one factor is that there are a lot of defensive mechanisms that were already in place but hadn’t really been tested.

Germany, in fact, has resorted to legislation in place to protect its strategic interests against hostile action by oil companies. This dates back to 1974 – not coincidentally, for that was just a year after the Arab oil embargo following the 1973 war with Israel. This same legislation was activated to counter the Kremlin’s attempt to convert energy dependence into political subservience after February 2022. And it worked just fine. The markets remember that.

A second factor is the rise of hydrocarbons production in North America. The US and Canada currently produce more oil and gas than the OPEC countries of the Middle East put together. That means that, thanks to the US “shale revolution” – so reviled in the EU – Europe’s transatlantic partners have plenty of oil and gas for themselves, and a certain amount to spare for their skeptical friends, when they need a little help.

It also means that North America, at least, is immune from one notable gap in the West’s defences, namely the impact of more than a decade of disinvestment in the oil and gas exploration and production sector. Europe, with its green obsessions, is obviously a lot less so.

But even Europe has done pretty well since February 2022 – perhaps surprisingly so. Though it’s in a rather more vulnerable position than North America, it’s nowhere near as vulnerable as it would have been quite recently. Consideration of how the EU and its members have performed in dealing with their energy situation since Mr Putin’s invasion is very instructive.

The EU responds

The key factor is that the EU’s politicians have not been hesitant about doing whatever was necessary for a rapid build-up of liquefied natural gas (LNG) infrastructure, ensuring the LNG underground gas storage facilities (UGS) were full, and buying whatever gas was needed from replacement sources, if necessary at a premium. Ukraine has sobered up the EU elite, prompting an overhaul of priorities and a willingness to spend money on defence and energy source diversification, a willingness to insist on the priority and urgency of relevant projects, and a willingness to brave the wrath of voters and consumers. These are not things that politicians can always be relied upon to do – and the fact that they have been doing them more from fear than from foresight hardly detracts from the results.

For those results are impressive. The EU currently has a regasification capacity of approximately 157 billion cubic metres per year (bcm/y), which is enough to meet around 40% of the EU’s total gas demand – and reflects the addition of 36.5 bcm/y since the start of 2022. That’s an increase of almost a third in less than two years.

The structure of natural gas imports has been altered radically, the two biggest winners from this being Norway (which in 2023 had a 24.3% share) and Azerbaijan (8.4%). The fact that the US supplied 12.8% of the EU’s gas consumption (45,6 bcm) illustrates another important truth: the EU is taking advantage of its enhanced LNG infrastructure and of abundant supplies the other side of the Atlantic (it is in fact the biggest customer for US LNG nowadays). Other non-Russian suppliers are Qatar (12,3 %) and Algeria (11.2%).

As to Russia, the figures are eloquent. According to Eurostat, in 2020 Russia accounted for 40% of the EU’s gas imports (or 28% of its consumption), while in 2023 the import share was just 27%. And imports of Russian gas by pipeline have, in absolute terms, dropped to less than a fifth of their former level – from 150 bcm to under 30 bcm.

Apart from good policy and determination, there’s been some luck too. The winter of 2022/23 was relatively warm. And there were no simultaneous energy shocks to deal with – none, that is, to compound the one caused by Mr Putin. And in the 2023-2024 season gas prices remain low due to high storage levels and moderate demand.

Energy consumption levels have worked in policy makers’ favour. They are down both in the household and in the industrial sector. This was partly due to successful adjustment to the shock of higher prices – a token of flexibility – but partly also to the facts that, in some sectors, demand has not yet recovered from the COVID-19 pandemic and that economic growth has been lower than expected.

And the energy mix has, in the event, worked out nicely. The EU is receiving increased amounts of electricity from renewable sources – so that “green obsession” we mentioned hasn’t been entirely without benefit – and, given moderate consumption, it has been able to keep coal-fired capacity largely as a reserve. Which means it’s been able to conserve its coal stocks. And, of course, there’s all that natural gas it has in storage.

A Red Sea crisis?

Moving on to how a prolonged Red Sea crisis – coming on top of reduced Russian oil and gas supplies – would affect the EU, I think the answer is that it might create a good deal of discomfort but would be far from devastating. For a start, the EU would be entering such a crisis with its general capacity for flexibility enhanced by the last couple of years’ experience; its stocks of fuel high (and all the higher for recent decisions raising the level of mandatory reserves); and the infrastructure it would need to import more from diverse sources much enhanced. Energy efficiency is on the up, renewables will continue to help, and so will the fact that energy demand is still low.

Of the gas import shares mentioned above, only Qatar’s gas comes through the Red Sea, and the opportunities for getting replacements on the world LNG market are abundant.

Oil is perhaps somewhat more problematic – since around 20% of the EU’s oil imports come via the Red Sea. But it should be remembered that, so far at least, oil flows via that route have only been reduced, not stopped. And there are easily accessible alternative sources: North America and Angola, to name but two, plus a lot of cargo swaps in the making.

And Russia! For there’s a beautifully ironic twist to be taken into account as well.

Oil and gas production is subject to inertia. It can’t be switched on and off instantly and at will. Stop an oil or gas well producing and there’s a fair chance you won’t be able to re-start it without heavy additional spending – or, perhaps, at all.

So, even though it has been short of markets, Russia has tended to keep pumping out oil and gas over the last couple of years and keeping some of the resultant output in its internal storage facilities. Stocks reached record levels in 2023 and there is now no room for further buffering.

Result: Russia is desperate to sell abroad and will become more so as time goes on.

Hoist on his own Petard

Given that it’s difficult to sell Russian oil in Europe, a good deal of it has been going south via Suez and the Red Sea lately. If that route becomes too dangerous, the oil in question will tend to stay north of Suez and try to find buyers there – in Egypt, perhaps, or Turkey, but also elsewhere in Europe. Legally or not, some will find its way through to the market. That’s less than optimal from the standpoint of Western policy-makers, since it means that Mr Putin will be deriving revenue from such sales. But it does mean that any shortages in Europe are likely in practice to be mitigated by Russian oil that ought not to be there in theory.

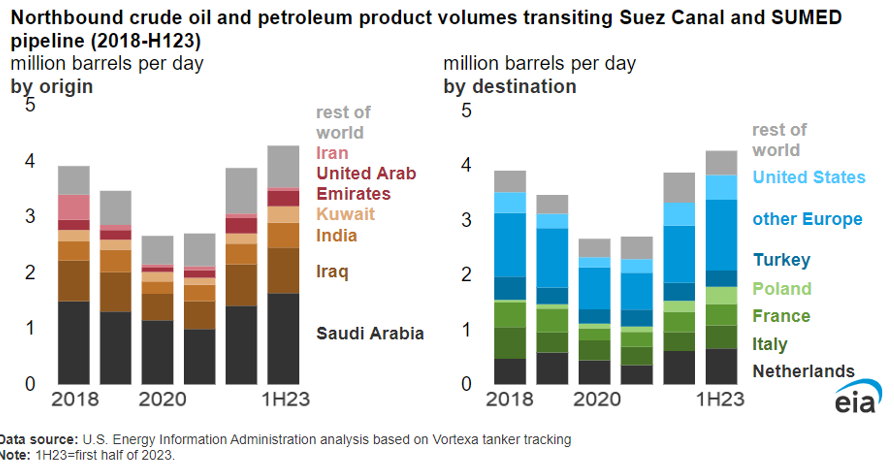

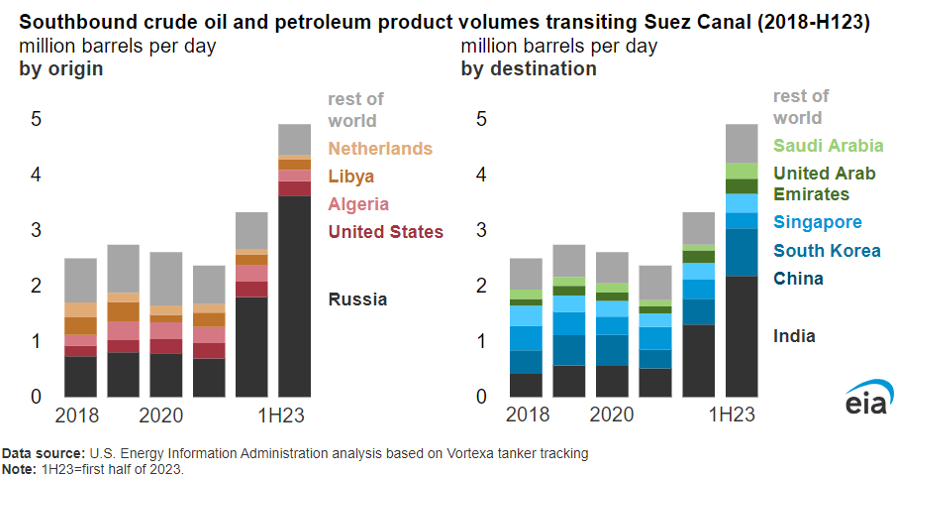

And, as A&A readers will certainly have inferred by now, the irony doesn’t stop there. Over 60% of crude oil traffic from the Mediterranean to the Red Sea nowadays is Russian. The Kremlin’s oil revenues depend on sales to India and Pakistan, along with swap deals with Saudi Arabia. So Russia is at least as vulnerable as the EU to trouble in the Red Sea.

Mr Putin may have been hoping to secure immunity by virtue of his links to the Houthis, as well as those of his allies the Iranians. Undertakings to that effect were announced at the end of a recent Houthi visit to Moscow – with immunity extending to Chinese as well as Russian vessels.

But even assuming perfect goodwill, there’s some implausibility to the idea that low-tech (though well-armed and determined) fighters like the Houthis will be able to tell which ships are Russian and which are carrying cargoes of Russian oil. And, to date, one Russian tanker has gone up in flames, while another tanker chartered by Singapore-headquartered Trafigura, Mr Putin’s favourite Western oil trader, has come under fire.

In short, a resilience threshold in the West that has been heightened since the 2022 invasion of Ukraine is preventing – and will prevent – Moscow from translating geopolitical stress either into serious problems for the West or into sustained oil and gas price increases. The most serious loser is likely to be Mr Putin himself.

And that’s even before we take into account the subject of the next part of this two-part article: the effects on his relations with various powers which he’d very much like to be, or remain, his friends.

Ilian Vassilev